What is valuation, why does it matter and how do we do valuation?

Introduction

By its very nature, valuation work cannot be regarded as an exact science and the conclusions arrived at in many cases will of necessity be subjective and dependent on the exercise of individual judgment. As such, two separate (and well qualified) valuation practitioners could come to different answers. Our task is to make sure the work delivered to you is as robust and defensible as possible, as we often will need to defend our position.

The demand for valuation work could come from financial reporting (i.e. impairment review, purchase price allocation and share options, etc. – these are our services priority), tax, project financing, dispute/ litigation, investment appraisal, restructuring and other regulatory requirements.

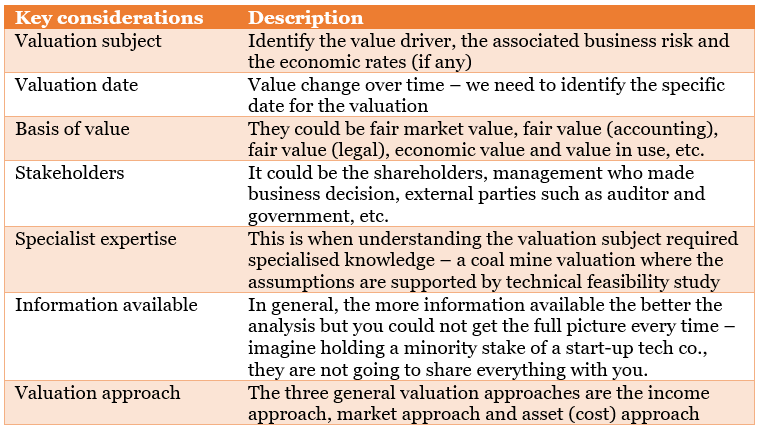

Plenty of key considerations when it comes to valuation works, they are key to how we perform any valuation work:

The following discussion points here are to give you a simple idea of why valuation matters and how the minor items could impact the final results.

1. Price versus Value

Price does not necessarily equal value.

Price is determined after putting the asset up for sale in the open market.

Value is determined in the context of a notional market at a point in time (current or historical). So you may ask, why do price and value deviate? This is because valuations do not necessarily capture the buyer and sellers unique situations (i.e. the operating and finance synergies, information availability, funds available for purchase, participant specific motivation).

Price can be influenced by affordability (does purchaser have enough cash and can they get financing for the acquisition?) and seller specific issues such as whether or not the Price can be influenced by affordability (does purchaser have enough cash and can they get financing for the acquisition) and seller specific issues such as whether or not the seller is in a rush to sell (i.e. forced sale). Value, on the other hand, is more in terms of what it is actually worth to the purchaser or seller after considering the above (i.e. synergies and information availability, etc.) Speaking of synergies, a real life example would be that the acquirer would be willing to pay a premium for the expected cost synergies (i.e. a leaner organisation) or the expected revenue synergies (i.e. increase in market size) subsequent to the acquisition.

During a merge and acquisition negotiation process, the purchaser will not give away all of their expected synergies) and the competitiveness of the bid could also influence the price. This explains why two separate valuation practitioners could reach two conclusions, i.e. with the buy-side (sell-side) advisors coming up with a lower value (higher value).

2. Enterprise value vs Equity value

My experience as an ex-auditor tell me that you may not be aware of the difference, as these terms, together, may not come up that often and they could be easily overlooked.

Equity value is the value directly attributable to the shareholders or owners of equity, i.e. the net asset value.

Enterprise value is the sum of claims of all the security-holders: debt holders, preferred shareholders, minority shareholders, common equity holders, and others. To put it in another way, the enterprise value is the sources of financing (i.e. net debt + equity value), or the assets of an entity (i.e. net working capital, fixed assets and other assets, etc.)

From an accounting perspective, equity value is equity, enterprise value is asset (i.e. equity + liabilities). Simple enough.

The reason why this matter will come later – the free cash flow to firm / free cash flow to equity

3. Level of value

The level of value, from top to bottom:

Strategic controlling basis > Financial controlling basis > Marketable minority basis > Non-marketable minority basis

Strategic controlling basis, as the name suggested, it is the value of an entity where strategic decision making could be obtained. It is the highest. This is closely related to the income approach (using the discounted future cash flow) or the market approach (using the guideline transaction method)

Financial controlling basis, simply put, is the value of, when an entity obtains over 50% of the shareholding and could exercise control (technically speaking it is when certain party has the power to control, according to the accounting standard). It comes off second of the list.

Marketable minority basis, is the value of an entity that is marketable (i.e. think of stocks that you could freely transfer in the open market such as a stock exchange), and is on a minority basis (i.e. again think of the stocks you held it is usually an ant-size relative to the entire share cap). This is closely related to the market approach (using the comparable quoted company multiples)

Non-marketable minority basis, is the value of a ‘private’ entity where one need to actively look for market participants to trade (concerning the liquidity of a transaction), and is on a minority basis (i.e. excel no control / significant influence on the entity).

The items that bridge the four basis are the control premium, discount for lack of control and discount for lack of marketability, and they are mostly down to professional judgement.

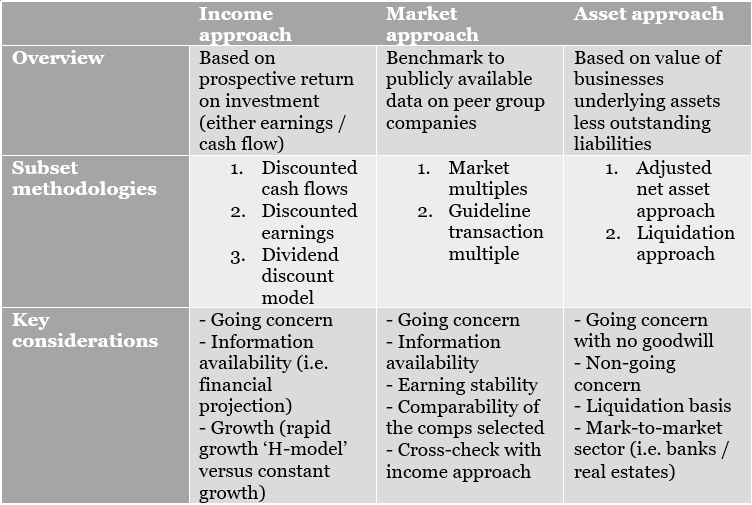

4. Valuation approach

At a glance:

Asset approach

Liquidation approach derives the ‘wind-up’ value of the business of say if all assets are sold and all liabilities are paid off, and at last the ‘proceed’ distributable to the owners. Disposal costs should be considered. It does not consider future earnings stream and is therefore merely the sum of the parts of an entity.

Adjusted net asset approach, considers assets ‘value-in-use’ rather than ‘liquidation value’, and as a sale of business as a whole as opposed to a liquidation. This is common for banks as the value is primarily derived from the tangible assets (i.e. cash, certificate deposits and stock investments, etc.)

Click on the following hyperlinks for details of income approach and market approach.